Experiencing medical hair loss from chemotherapy, alopecia, or trichotillomania is deeply personal. For many, finding a beautiful, natural-looking hair replacement is an empowering step toward feeling like themselves again. But while many local residents begin their journey by simply looking for the best wig stores in Columbus Ohio for aesthetic reasons, those facing medical hair loss encounter an entirely different landscape: navigating the complex world of health insurance claims.

If you are just beginning to explore your options, you might be wondering if your health insurance will help cover the costs. The short answer is yes—but the process requires a very specific approach. Because insurance companies rely on exact terminology and medical codes, securing financial assistance for a medical wig can feel overwhelming.

Think of this guide as a knowledgeable friend walking you through the process step-by-step. We’ll demystify the insurance jargon, highlight the exact documentation you need, and point you toward trusted Columbus-area boutiques that understand how to help you secure the coverage you deserve.

The Golden Rule: It Is Never a “Wig”

When it comes to health insurance, terminology is everything. To an insurance company’s computerized system, the word “wig” implies a luxury or purely cosmetic item, triggering an automatic claim denial.

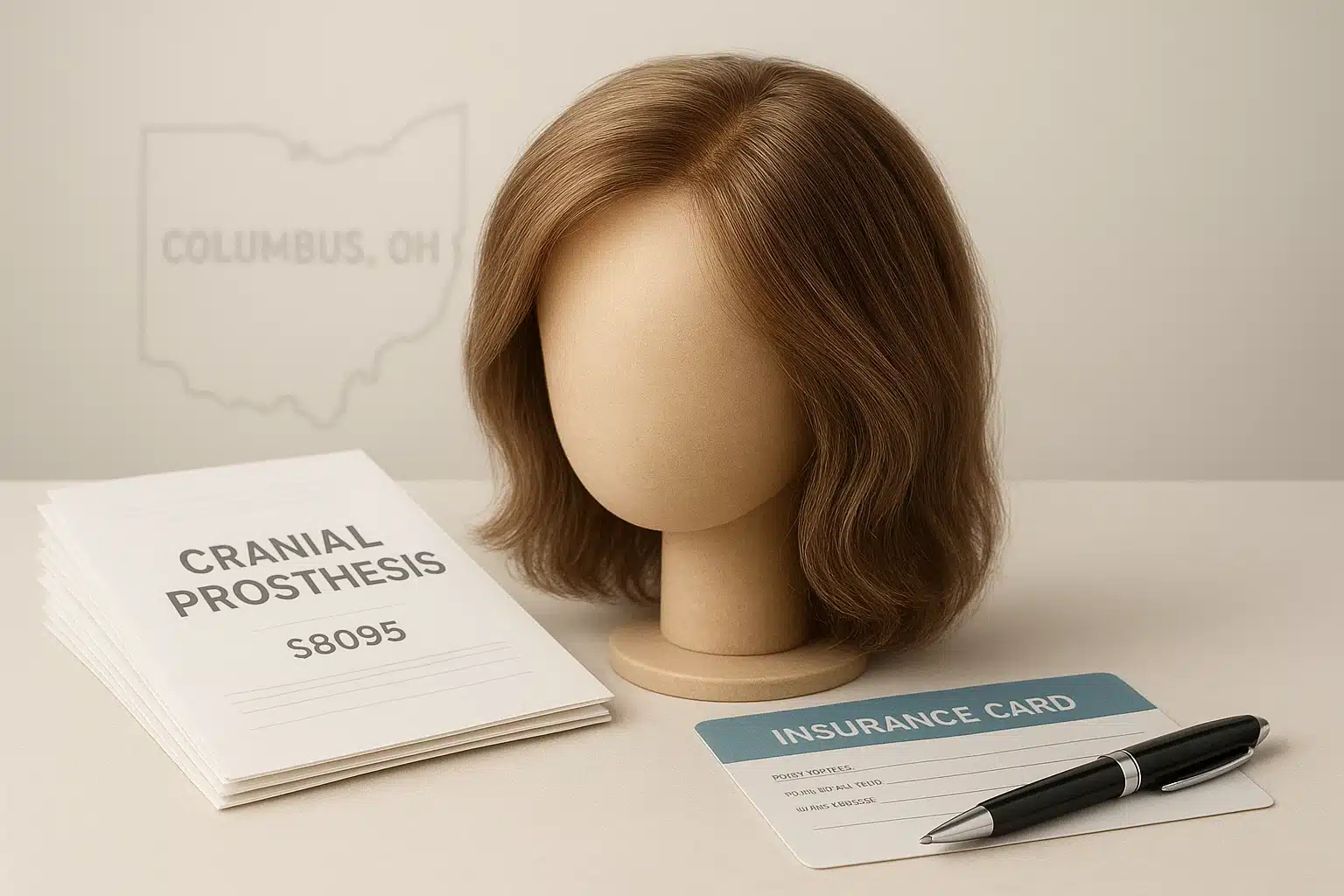

To secure medical reimbursement, you must use the term cranial hair prosthesis (or cranial prosthesis). This specific language shifts the classification of your hairpiece from a cosmetic accessory to Durable Medical Equipment (DME), which is covered under many health insurance policies.

Keep this golden rule in mind: The word “wig” should never appear on your prescription, your letter of medical necessity, or your final boutique invoice.

Essential Medical Codes to Know

When you visit your doctor, they will need to include specific codes on your paperwork to prove your cranial prosthesis is medically necessary. Having these codes handy can save you hours of back-and-forth communication later.

HCPCS Billing Codes (What the item is):

- S8095: Wig, prescribed, synthetic or human hair (This is the primary billing code used for private insurance).

- A9282: Wig, any type, stimulating/cooling/cranial prosthesis.

ICD-10 Diagnosis Codes (Why you need it):

- C96.9: Chemotherapy/Oncology-induced alopecia

- L63.9: Alopecia Areata

- L63.0: Alopecia Totalis

- F63.3: Trichotillomania (Compulsive hair pulling)

- L65.9: Medical Hair Loss / Alopecia, unspecified

Note: Cosmetic additions, such as hair extensions or cosmetic toppers, are strictly viewed as aesthetic enhancements and will not be covered under DME benefits, regardless of your diagnosis.

Your Step-by-Step Claim Roadmap

Building a bulletproof insurance claim doesn’t have to be intimidating. By gathering the right documents in the right order, you can confidently submit your claim for reimbursement.

- Obtain a Specifically Worded Prescription: Ask your oncologist, dermatologist, or primary care physician for a prescription. It must explicitly state: “Cranial prosthesis for medical hair loss due to [Insert Diagnosis / ICD-10 Code].”

- Request a Letter of Medical Necessity (LMN): Along with the prescription, your doctor should write a brief letter detailing the physical need (such as skin/scalp vulnerability) and psychological distress caused by your condition.

- Schedule a Consult at a Medical-Grade Boutique: Work with a specialized salon that understands medical hair loss and provides itemized medical invoices.

- Audit Your Invoice: Before you leave the boutique, ensure your final invoice lists the store’s Federal Tax ID, their NPI code (if applicable), the billing code S8095, and the description “Cranial Hair Prosthesis.”

- Submit the Claim: File the completed claim form, your doctor’s LMN, the prescription, and your itemized invoice directly to your insurer’s DME department.

Carrier-Specific Policies for Ohio Residents

Insurance policies vary wildly. While states like California and Texas have mandates requiring minimum coverage levels for oncology patients, Ohio relies on the specifics of your individual or employer-sponsored group plan. Here is a look at how major carriers typically handle cranial prosthesis claims:

- Anthem Blue Cross Blue Shield (BCBS) of Ohio: Anthem generally covers cranial prostheses under most group plans, primarily for oncology or severe accidental hair loss. You’ll want to check your specific plan’s DME cap, which commonly ranges from $350 to $1,000 per calendar year.

- Aetna: Coverage is generally provided if a DME rider exists on your plan. Aetna’s policy (CPB 0423) strictly guides medical necessity, requiring documented chronic alopecia or cancer therapies.

- TRICARE: Serving our military families, TRICARE is highly strict but very reliable. They cover exactly one hairpiece per beneficiary per lifetime up to standard allowances, provided the hair loss is a direct result of active oncology treatments or specific congenital/injury diagnoses. (Note: Standard androgenetic hair loss is explicitly excluded).

- UnitedHealthcare (UHC): Group plans often cover up to 80% of the S8095 code, though many regional Ohio plans require you to secure prior authorization before making your purchase.

Columbus, OH Directory: Insurer-Friendly Boutiques

Finding a local shop that understands the emotional weight of medical hair loss—and the logistical headache of insurance—is crucial. Here are several Columbus-area resources equipped to help medical patients:

Over My Head Cancer Boutique

- Location: Inside the Bing Cancer Center (500 Thomas Lane, Suite 1A, Columbus, OH)

- Why they stand out: Nestled directly inside the OhioHealth oncology hub, this boutique is a patient-first resource. Their seasoned staff specialize exclusively in medical hair loss and can walk cancer patients through the exact insurance processes.

Van Scoy Hair Clinics

- Location: 4280 Clearwater Dr, Columbus, OH

- Why they stand out: Van Scoy is a longstanding Ohio authority for custom cranial prosthetics, alopecia solutions, and medical-grade human hair systems. They are well-versed in providing the detailed, itemized medical billing paperwork insurers require.

Bio Medic Hair Systems Inc

- Location: Columbus, OH

- Why they stand out: Specializing in non-surgical medical hair replacements, this is an excellent resource for long-term alopecia and trichotillomania prosthetics.

Luxe Hair Solutions

- Location: Powell, OH (Northwest Columbus area)

- Why they stand out: Operating out of private suites tailored to medical patients, they offer thorough, compassionate guidance on compiling the exact documentation needed for insurance reimbursement.

A Helpful Time-Saver

When you are calling local salons, it’s just as helpful to know who doesn’t handle medical billing so you can save your energy. For example, local shops like Stephanie’s Salon LLC offer wonderful cosmetic services but explicitly state they do not accept insurance or participate in DME billing.

What to Do If Your Claim Is Denied

Don’t panic if your initial claim is rejected. Denials are incredibly common and are usually the result of an automated computer system catching a minor clerical error.

If you receive a denial, review the paperwork you submitted. Did the word “wig” slip onto the boutique’s invoice? Did the doctor forget the ICD-10 code? Simply correct the paperwork, attach a brief explanation clarifying that the item is a prescribed cranial prosthesis for a medical condition, and submit it through your insurance company’s formal appeals process.

Frequently Asked Questions (FAQ)

Does health insurance cover hair loss due to natural aging?

No. Standard androgenetic alopecia (pattern baldness or thinning hair due to age and genetics) is not considered a medical necessity by insurance providers. Coverage is reserved for disease-induced hair loss (like alopecia areata), medical treatments (like chemotherapy), or trauma.

Will my insurance pay the boutique directly?

In most cases, no. Cranial prostheses typically operate on a reimbursement model. You will usually pay the boutique out-of-pocket for your hairpiece, and then submit your audited invoice and medical documents to your insurance company to be reimbursed directly by check.

Does my insurance cap how much they will pay?

Yes. Most insurance plans have a DME allowance cap per calendar year or per lifetime. For example, your plan might pay 80% of the cost up to $500. It is highly recommended to call the number on the back of your insurance card and ask specifically about your “Durable Medical Equipment coverage for a cranial prosthesis” before you shop.

Can I buy a medical wig online and still get reimbursed?

Yes, as long as the online retailer can provide you with an itemized invoice containing their Tax ID and the correct HCPCS code (S8095). However, visiting a local Columbus boutique allows you to have the piece professionally fitted and styled, which is incredibly important for sensitive scalps undergoing medical treatments.

Taking Your Next Steps

Navigating medical hair loss is a journey, and you don’t have to walk it alone. By arming yourself with the right terminology, working closely with your doctor to secure a Letter of Medical Necessity, and partnering with an experienced Columbus boutique, you can ease the financial burden of hair replacement.

Take it one step at a time. Start by speaking with your doctor about your prescription, and then reach out to a local specialist to begin exploring the beautiful, comfortable cranial prostheses available to you.