Experiencing hair loss due to chemotherapy, alopecia, trichotillomania, or lupus brings a wave of emotional and physical challenges. Regaining your confidence shouldn’t mean draining your savings. If you are beginning this deeply personal journey, you have likely started by looking into wig stores in Albuquerque in hopes of finding a specialized, compassionate environment to help you look and feel like yourself again.

However, finding a beautiful, comfortable hairpiece is often only half the battle. Navigating the complex intersection of health insurance, Medicaid, VA benefits, and flexible payment plans remains a major barrier for many. Too often, patients assume they can simply walk into a local boutique, hand over their insurance card, and walk out with a fully covered wig. The reality of medical billing is a bit more intricate, but highly manageable once you know the rules.

This guide will demystify the insurance process, reveal the financing strategies available to you, and provide a step-by-step roadmap to securing a premium medical wig with minimal out-of-pocket stress.

The Nomenclature Pivot: Why You Should Never Say “Wig” to Your Insurance Company

The single most important secret to unlocking insurance coverage is understanding medical terminology. To you and your loved ones, it’s a wig. To your health insurance provider, “wig” is synonymous with a cosmetic fashion accessory—and cosmetic accessories are automatically denied.

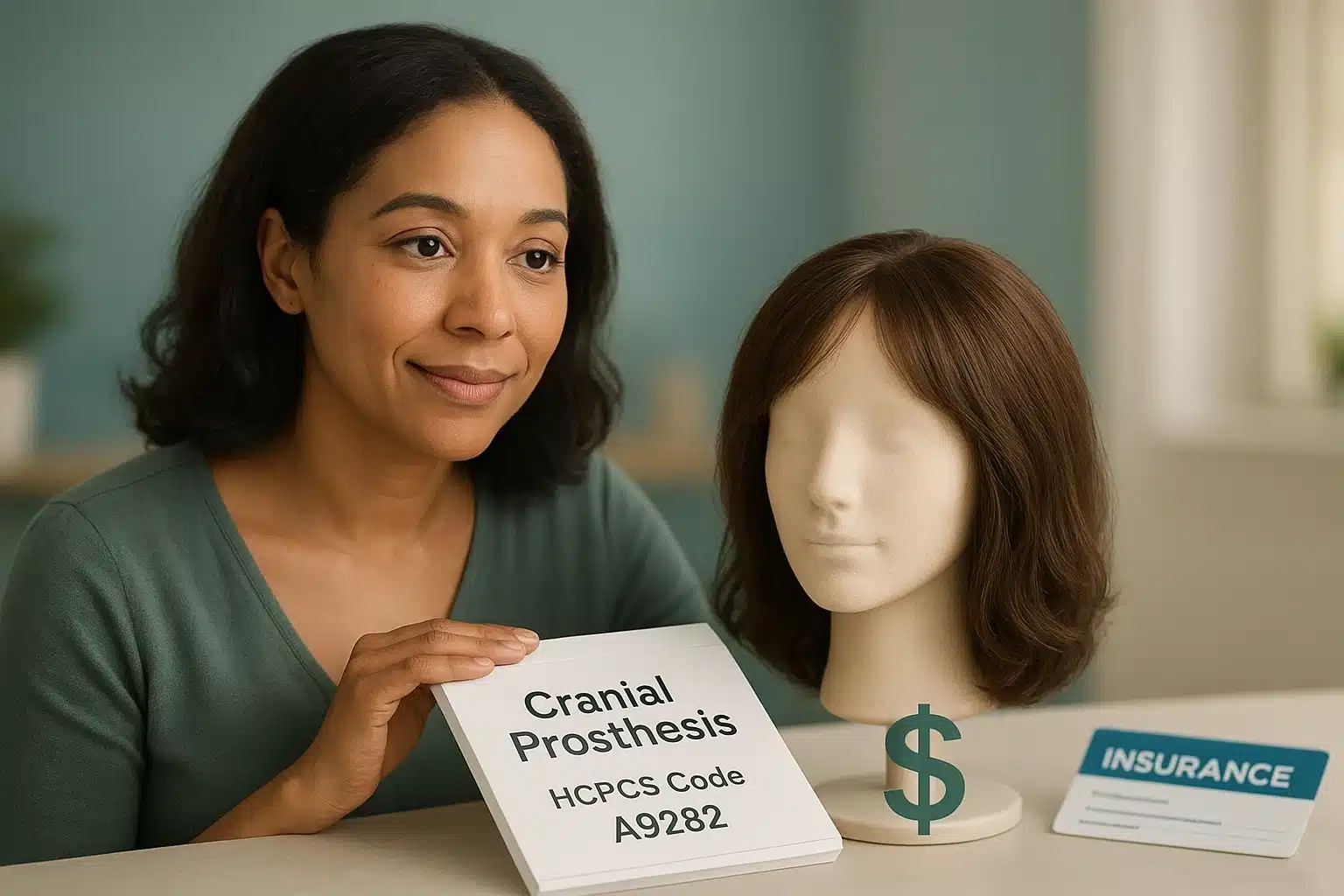

When seeking coverage, you are looking for a cranial prosthesis.

A true cranial prosthesis is engineered specifically for individuals with total or partial hair loss. Unlike standard fashion wigs, these medical-grade pieces feature specialized cap constructions, such as soft, hand-tied monofilament tops that won’t irritate a sensitive scalp during chemotherapy.

To get your insurance to pay, your doctor must write a prescription specifically for a “Cranial Prosthesis for medical purposes” and include the vital medical billing identifier: HCPCS Code A9282. Memorize this code; it is the golden key to your reimbursement.

The Albuquerque Insurance Landscape: Who Covers What?

Coverage varies wildly depending on your specific provider and plan. Here is a breakdown of what Albuquerque residents can generally expect from major local and national networks:

Commercial Insurance (Presbyterian & BCBS of New Mexico)

Many regional HMO and PPO plans offer robust support, but you must look closely at your Summary Plan Description. For example, some specialized group policies under Presbyterian Health Plan may provide maximum allowances of up to $3,000 annually for a cranial prosthesis, provided you secure pre-authorization first. Always ask about your specific deductible and out-of-network benefits.

TRICARE and Veterans Affairs (VA) Benefits

For military families, TRICARE typically covers exactly one cranial prosthesis per lifetime for beneficiaries experiencing hair loss due to radiation or chemotherapy, though an attending physician’s certification is required. Meanwhile, Albuquerque veterans can often obtain high-quality medical wigs directly through the local Raymond G. Murphy VA Medical Center’s Prosthetics Department at no out-of-pocket cost.

Medicare and New Mexico Medicaid

It is crucial to know that Original Medicare (Parts A and B) explicitly excludes coverage for wigs, categorizing them as cosmetic. However, if you are enrolled in a Medicare Advantage (Part C) plan, or certain New Mexico Medicaid Managed Care Organizations (like Turquoise Care), you may have supplemental benefits that offer partial or full coverage.

Exposing the “Direct-Billing” Myth

One of the most common points of friction for Albuquerque shoppers is a misunderstanding of how local shops handle insurance. You might see a boutique advertise that they “accept insurance,” leading you to believe you’ll only owe a standard $20 co-pay at the register.

The reality is different. Most boutique wig shops are classified as out-of-network Durable Medical Equipment (DME) providers. This means they do not bill your insurance directly. Instead, you are required to pay for the piece upfront. The shop will then provide you with a medically coded, itemized receipt containing your diagnosis code and HCPCS Code A9282. You will submit this receipt to your insurance company, who will then mail you a reimbursement check.

The Financial Bridge: How to Manage the Cash Gap

Premium human hair medical wigs can cost upwards of $1,000 to $3,000. If you have to pay upfront and wait 30 to 60 days for an insurance reimbursement check, how do you bridge that cash-flow gap? Modern financial tools make this highly accessible:

Using HSA and FSA Accounts

If you have a Health Savings Account (HSA) or Flexible Spending Account (FSA), you can use your tax-free funds to pay for your cranial prosthesis directly. Because it is a prescribed medical necessity, the purchase—and even ongoing wig maintenance supplies—are eligible expenses.

Buy Now, Pay Later (BNPL) Strategies

Many online retailers and modernized local shops now integrate BNPL services like Affirm, Shop Pay, or PayPal Credit. These services act as a “bridge loan.” You can break a $1,200 purchase into manageable $100 monthly installments. By the time your second or third installment is due, your out-of-network reimbursement check from your insurance company should have arrived, allowing you to pay off the balance effortlessly.

Step-by-Step: Securing Your Insurance Reimbursement

To ensure your claim sails through the administrative process without a hitch, follow this chronological action plan:

- The Doctor’s Visit: Ask your oncologist or dermatologist for a prescription. Crucial: Ensure it explicitly states “Cranial Prosthesis,” includes your specific diagnosis code (e.g., L63.9 for Alopecia Areata or C50.9 for Breast Cancer), and notes HCPCS code A9282.

- The Insurance Call: Before shopping, call the number on the back of your insurance card. Ask exactly: “Does my policy cover a cranial prosthesis under HCPCS code A9282? Do I have out-of-network DME benefits? Is pre-authorization required?”

- The Purchase: Whether shopping at a local Albuquerque boutique or a trusted online retailer, inform them you are buying a medical piece. You must leave with an itemized receipt showing the tax ID of the business, the medical code, and a description of the prosthesis.

- Submitting the Claim: Send your insurance company the itemized receipt, the doctor’s prescription, and a completed out-of-network claim form.

- Overcoming Denials: If your first claim is denied, don’t panic. Insurance companies frequently auto-deny these claims. File an appeal with a “Letter of Medical Necessity” from your doctor explaining the psychological and physical need for the prosthesis.

Frequently Asked Questions

What is the difference between a fashion wig and a medical wig?

Fashion wigs are created for cosmetic style changes and often feature heavy, machine-wefted caps. Medical wigs (cranial prostheses) are designed specifically for sensitive scalps lacking hair. They utilize ultra-soft materials, hand-tied knots for natural movement, and specialized linings (like polyurethane strips) to securely grip the scalp without the need for hair clips.

How much does a cranial prosthesis typically cost?

Prices range significantly based on materials. High-quality synthetic medical wigs generally range from $300 to $800, offering excellent style memory and easy maintenance. Premium 100% human hair prostheses, which offer maximum versatility and longevity, typically range from $1,000 to over $3,000.

Can I buy a medical wig online and still get reimbursed?

Absolutely. As long as the online retailer can provide you with an official, itemized receipt containing their tax ID and the necessary medical billing codes, your insurance company will process it the same way they would a receipt from a local Albuquerque store.

Taking the Next Step

Losing your hair is a profound transition, but finding a beautiful, confidence-restoring solution shouldn’t add financial trauma to your plate. By understanding the language of insurance, leveraging flexible payment plans, and treating your purchase as the vital medical equipment it is, you can take control of the process.

Take a breath, secure your prescription, and know that there are compassionate experts and financial pathways ready to support you every step of the way.