Experiencing hair loss due to chemotherapy, alopecia, or an autoimmune condition is a deeply personal and often overwhelming journey. The last thing you need during this vulnerable time is to fight with your insurance company over the coverage of a medical hair replacement system. Yet, here is a reality many patients discover the hard way: the difference between an outright denial and full financial coverage often comes down to just two specific words on a piece of paper.

Navigating this administrative maze can feel like trying to learn a foreign language overnight. Before you make a high-cost purchase, reviewing a complete guide to medical wig insurance coverage and financing is a crucial first step to understanding your out-of-pocket liabilities and benefits. Let’s decode the medical terminology, billing codes, and specific physician requirements you need to secure an insurance-ready prescription so you can focus on what truly matters—feeling like yourself again.

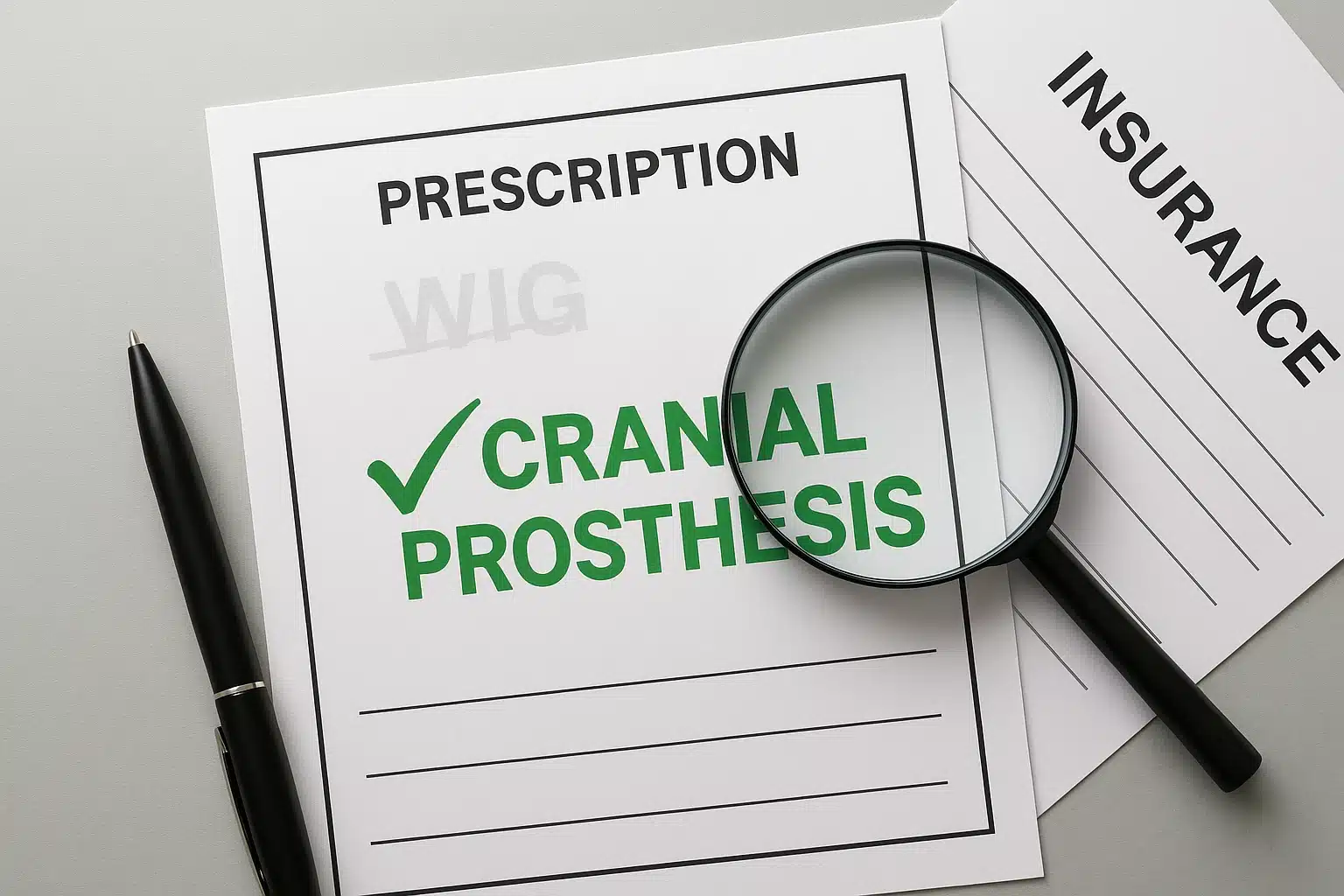

The “Two-Word” Difference Between Approval and Denial

The single most common reason insurance claims for medical hair systems are denied is the terminology used on the prescription.

Insurance claims are processed by automated software systems programmed with strict filters. If the keyword “wig” is detected anywhere on your prescription or the primary fields of your CMS-1500 insurance claim form, the system instantly routes it to a “cosmetic exclusion” pile. To an insurance computer, a wig is a fashion accessory.

To bypass this automated rejection, your doctor must use the term “Cranial Prosthesis” or “Cranial Hair Prosthesis.” This specific phrasing instantly reclassifies the item from a cosmetic luxury to a piece of Durable Medical Equipment (DME) required for your well-being.

The Anatomy of an Insurance-Ready Prescription

A quick note jotted down on a prescription pad won’t pass an insurance audit. Your prescription needs to be a highly specific medical blueprint.

The Specialty Rule

While your primary care physician can write a prescription, documentation from a specialist carries significantly more weight with medical review boards. If you want to maximize your chances of approval, get your script from the specialist treating your underlying condition:

- Oncologists for chemotherapy-related hair loss

- Dermatologists for Alopecia Areata or scarring alopecias

- Endocrinologists for thyroid-induced or autoimmune hair loss

Administrative Essentials

Before leaving the doctor’s office, check that your prescription includes these non-negotiable details:

- The physician’s National Provider Identifier (NPI) number

- The clinic’s Tax ID or Employer Identification Number (EIN)

- A clear, non-expired signature and current date

- A specific diagnosis code (ICD-10) and procedure code (HCPCS)

Your Medical Coding Blueprint (The Cheat Sheet)

If you’re wondering how to ask your doctor for a prescription wig, the best approach is to bring the exact codes they need right to your appointment. Doctors are incredibly busy, and having this “cheat sheet” ready ensures your paperwork is flawless.

Insurance companies require two types of codes to process a claim: the HCPCS Code (what the item is) and the ICD-10 Code (why you need it).

Step 1: The HCPCS (Procedure) Codes

Ensure your doctor selects the code that matches the exact type of prosthesis you are purchasing. A code mismatch is a guaranteed denial.

- A9282 (Wig, any type, each): This is the universal standard code used for high-quality synthetic cranial prostheses or ready-to-wear medical pieces.

- S8095 (Cranial prosthesis, other than temporary, custom-designed): This code should strictly be used for custom-fit, 100% human hair prostheses.

- L8499 (Unspecified prosthetic procedure): Sometimes used as a fallback code for specific private insurers with unique billing structures.

Step 2: The ICD-10 (Diagnosis) Codes

Your doctor will need to pair the item code with the medical reason for your hair loss:

- For Chemotherapy Patients: Ask your doctor to use Z92.21 (Personal history of antineoplastic chemotherapy) alongside L65.9 (Nonscarring hair loss, unspecified).

- For Alopecia Areata Patients: The most common codes are L63.9 (Alopecia areata, unspecified) or L63.0 (Alopecia totalis).

- For Autoimmune/Thyroid Patients: Often billed as E03.9 (Hypothyroidism, unspecified) paired with L65.9.

Navigating Retailer Invoices, Payments, and Medicaid

Once you have the perfect prescription, your journey transitions to the retailer. The invoice provided by your wig supplier must be a mirror image of your doctor’s prescription.

The “Before You Buy” Audit:

- Does the invoice say “Cranial Prosthesis” instead of wig?

- Does it include the correct HCPCS code (e.g., A9282)?

- Does it list the retailer’s Tax ID?

Managing Out-of-Pocket Costs

Medical cranial prostheses require upfront payment, meaning you will face initial wig prescription charges while you wait for your insurance reimbursement. If the upfront cost is a barrier, look into alternative financial solutions. You can frequently utilize HSA (Health Savings Account) or FSA (Flexible Spending Account) funds. Additionally, many trusted retailers offer financing solutions that allow you to pay monthly for a wig, easing the immediate financial burden.

If you are on state assistance, search for specific “medical card wig” pathways in your state. Medicaid coverage for cranial prostheses varies heavily by region, but many states do offer partial or full reimbursement for patients under age 21 or those with specific medical diagnoses.

Beyond the Prescription: Caring for Your Medical Prosthesis

A true medical-grade cranial prosthesis is fundamentally different from a fashion wig. They are meticulously crafted with hypoallergenic bases, monofilament tops, and hand-tied knots designed to protect sensitive, compromised scalps. Because of this delicate construction, treating them requires immense care.

If you opt for a human hair medical system and want to customize the color, learning how to tone a wig safely is critical. You must use gentle, acid-balanced toners and carefully avoid the base, as harsh chemicals can easily dissolve the delicate hand-tied knots. Furthermore, if you need to know how to style a wig without a wig stand, always lay it flat on a soft, clean towel. Pulling or stretching the cap over a makeshift stand can warp the specialized silicone grips or tear the delicate French lace designed to hug your scalp.

What to Do if You Get Denied: The Step-by-Step Appeal

Even with perfect paperwork, automated systems sometimes issue a denial. Do not panic—this is incredibly common, and appeals are highly successful when handled correctly.

If you receive a denial, you will need to submit a Letter of Medical Necessity (LMN) written by your treating physician.

LMN Copy-Paste Builder Requirements for Your Doctor:

- Patient History: “I am writing on behalf of [Your Name], who is currently undergoing treatment for [Condition/Diagnosis].”

- Medical Justification: “Due to this treatment, the patient suffers from severe alopecia. A cranial prosthesis is not for cosmetic purposes but is medically necessary to regulate body temperature, protect the compromised scalp from UV radiation, and prevent severe psychological distress that could hinder the healing process.”

- Action Request: “Please review this claim for a Durable Medical Equipment (DME) cranial prosthesis under HCPCS code [Insert Code].”

Frequently Asked Questions (FAQ)

Will my insurance cover a wig?

Many private insurance companies will cover a medical wig, but they will never cover it if it is billed as a “wig.” It must be prescribed and billed as a “cranial prosthesis” or “extra-corporeal hair prosthesis.” Coverage limits depend entirely on your specific policy’s Durable Medical Equipment (DME) benefits.

How do I ask my doctor for a wig prescription?

Be direct and bring the requirements with you. Say, “My hair loss is affecting my daily life and recovery. I am purchasing a cranial prosthesis, and my insurance requires a prescription containing specific HCPCS and ICD-10 medical codes. I have a list of the required formatting here—could we draft this today?”

Why does my invoice have to say “cranial prosthesis” instead of “wig”?

Insurance claim software uses keyword filters. The word “wig” triggers an automatic denial because it is categorized as a cosmetic accessory. “Cranial prosthesis” flags the item as necessary medical equipment.

Can I use a state medical card or Medicaid for a wig?

It depends on your state. Some state Medicaid programs cover cranial prostheses for specific medical conditions or age groups (often under 21). You will need to check your state’s specific Medicaid DME guidelines.

Your Next Steps Toward Confidence

Navigating medical hair loss is a profound challenge, but dealing with insurance doesn’t have to be. By understanding the precise wording, the specific diagnostic codes, and the structural differences of medical-grade pieces, you are now equipped to advocate for yourself effectively.

Armed with this knowledge, you can confidently approach your doctor, secure your prescription, and find a high-quality cranial prosthesis that helps you look and feel beautifully like yourself again. Take the time to print out the code blueprints, prepare for your next appointment, and remember that compassionate experts are always available to help guide you through the rest of your journey.