Losing your hair to chemotherapy, alopecia, or scalp trauma is an incredibly emotional experience. It’s not just about aesthetics; it’s about feeling like yourself again during a deeply vulnerable time. When you’re managing a diagnosis, the very last thing you want to worry about is how to afford a medical-grade wig. Finding compassionate support and knowing where to start your search is crucial, which is why locating a reputable wig store New Orleans residents trust for sensitive medical fittings is often the vital first step toward recovery and regaining your confidence.

Unfortunately, the path to obtaining insurance coverage for these essential items is often paved with confusing terminology, complex billing codes, and localized bureaucratic hurdles. Many families mistakenly assume their insurance card can be run at the register like a standard pharmacy prescription, only to be met with unexpected out-of-pocket costs and frustrating claim denials.

But here is the good news: getting your health insurance to cover a medical wig is entirely possible when you know the rules of the game. Let’s demystify the process and explore exactly how to navigate insurance claims, decode the paperwork, and find localized support right here in the Crescent City.

The Medical Vocabulary Pivot: Why Words Matter to Insurance Adjusters

The most common reason insurance claims are denied has nothing to do with your medical need and everything to do with vocabulary.

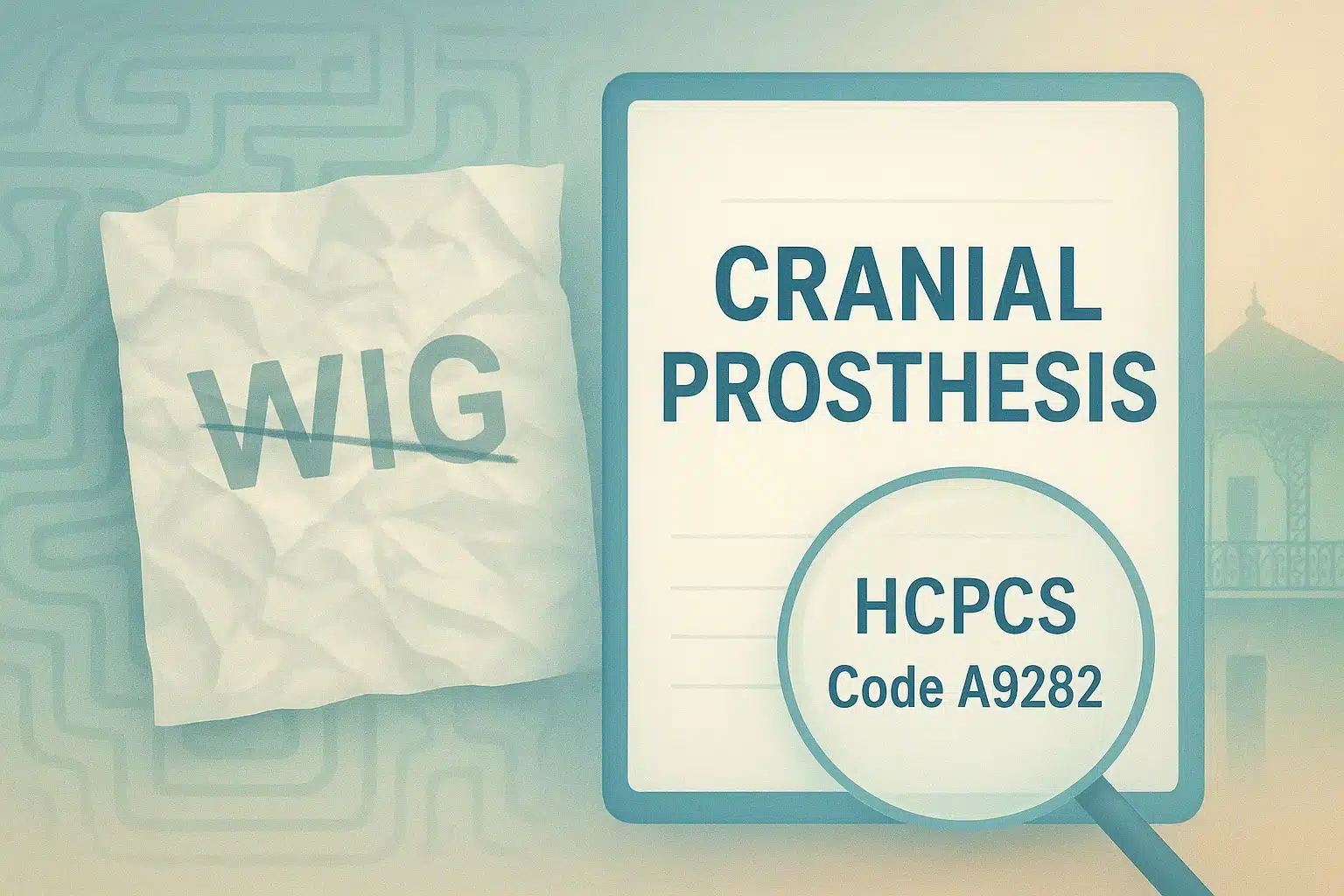

Here is the biggest “aha moment” for navigating medical hair loss: Insurance companies routinely deny claims containing the word “wig.” In the eyes of an insurance adjuster, a “wig” is classified as a cosmetic fashion item. To bypass automated denials, your documentation must use the correct clinical terminology. The secret password is Cranial Prosthesis (or Cranial Hair Prosthesis/Scalp Prosthesis).

To speak the insurance company’s language fluently, you’ll need to familiarize yourself with two specific types of clinical codes:

- HCPCS Code A9282: This is the universal medical coding standard for a synthetic or human hair cranial prosthesis.

- ICD-10 Diagnosis Codes: These are the codes your doctor uses to explain why you need the prosthesis. Common examples include L65.9 (Alopecia, unspecified) or secondary oncology codes representing chemotherapy-induced hair loss.

Step-by-Step: How to Secure Your Insurance Coverage

Securing coverage doesn’t have to be a guessing game. By following a structured chronological path, you can eliminate the costly surprises that catch many patients off guard.

Step 1: Contact Your Insurer to Check “DME” Benefits

Before buying anything, call the number on the back of your insurance card. Don’t ask if they cover wigs. Instead, ask: “Does my policy include coverage for Durable Medical Equipment (DME)? Specifically, I am looking to see if HCPCS Code A9282 for a cranial prosthesis is covered.” Write down the name of the representative, the date, and the reference number for the call.

Step 2: Obtain the Right Prescription and Letter of Medical Necessity

You will need a prescription and a Letter of Medical Necessity (LMN) from your oncologist or dermatologist. Because doctors are incredibly busy, they sometimes write “wig for cancer patient” on the script out of habit, which will trigger an automatic denial.

Your Doctor-to-Patient Scripting Template:Feel free to copy, paste, and hand this directly to your doctor:

“Please write the prescription for a ‘Cranial hair prosthesis for medical purposes secondary to chemotherapy-induced alopecia (ICD-10: [Insert Your Code]).’ Please do not write the word ‘wig’ on any part of the prescription or Letter of Medical Necessity.”

Step 3: Navigate the “Prepayment” Surprise

Most general guides gloss over a harsh reality: medical wigs must almost always be prepaid out-of-pocket by the patient. You will purchase the cranial prosthesis upfront and then file a claim with your insurance company for retroactive reimbursement. Ask your provider for a highly detailed receipt that includes the shop’s Tax ID number, your name, the phrase “Cranial Prosthesis,” and the A9282 code.

Louisiana Insurance Deep Dive: Blue Cross Blue Shield & Medicaid Rules

If you are navigating New Orleans insurance networks, there are localized rules that directly impact your coverage.

The Deductible Trap

If you have a private carrier like Blue Cross Blue Shield of Louisiana, you might be thrilled to hear that your plan covers cranial prostheses at 80%. However, be aware of the “Deductible Trap.” Because a cranial prosthesis falls under Durable Medical Equipment (DME), you must meet your annual DME deductible before that 80% coverage kicks in. Always ask your insurer how much of your deductible you have already met for the year.

The Louisiana Medicaid Myth-Buster

There is a massive contradiction in search results regarding Medicaid in Louisiana. Broad legal statutes from years past state that state programs do not reimburse for wigs. However, if you look closely at the Louisiana Department of Health’s official Medicaid Managed Care Policies & Procedures, they do allow coverage for “cranial hair prostheses” under code A9282 when deemed medically necessary. If you are on Medicaid, work closely with your social worker to ensure your Letter of Medical Necessity is airtight, as coverage is absolutely possible under current guidelines.

Local New Orleans Resources: Finding Support When You Need It Most

Sometimes, despite your best efforts, insurance falls short. If your claim is denied, or if you simply need hands-on, empathetic support, New Orleans has a robust network of resources ready to help.

Hospital Wig Clinics and Support Groups

Local health systems offer incredible on-the-ground support. LCMC Health, for instance, frequently hosts a Patient Support & Wig Clinic Program. These monthly events often provide oncology patients with free styling, custom fittings, and a safe space to connect with others on a similar journey. Oncology social workers at Ochsner Medical Center and Touro Infirmary can also connect you with local hospital wig banks that offer donated, gently used, or brand-new prostheses at no cost.

Filing a Gap Exception

If you have private insurance but cannot find an “in-network” medical wig provider within a 50-mile radius of New Orleans, you can file what is called a “Gap Exception.” This legally forces your insurance company to cover an out-of-network specialized shop at the in-network rate, ensuring you don’t have to settle for a provider who doesn’t understand the complexities of a sensitive, post-chemotherapy scalp.

Frequently Asked Questions

Are wigs for cancer patients covered by insurance?

Yes, in many cases they are. However, they are covered under the Durable Medical Equipment (DME) portion of your health insurance policy, and they must be prescribed and billed as a “Cranial Prosthesis” rather than a wig.

What is the medical term for a wig?

The globally recognized medical terms used for insurance billing are Cranial Prosthesis, Cranial Hair Prosthesis, or Scalp Prosthesis.

How do I get my doctor to write a prescription for a wig?

Simply ask your oncologist or dermatologist during your consultation. Bring the exact terminology and billing codes (HCPCS Code A9282) with you to ensure the prescription is written in a way that your insurance company will accept on the first try.

Taking Your Next Steps

Navigating medical hair loss is a journey that requires patience, self-compassion, and the right information. By understanding the vocabulary of insurance adjusters, knowing your local Louisiana policies, and tapping into New Orleans’ incredible community resources, you can transform a stressful logistical barrier into an empowering pathway to care.

Take it one step at a time. Start by checking your DME benefits, securing your medical documentation, and reaching out to specialized local providers who understand that finding the right cranial prosthesis isn’t just about how you look—it’s about how you feel.